Evan does a nice job at saying “it depends”, gives us the math and then tells the story of a gentleman, who had $5MM of assets and no liabilities, who dropped “a significant amount” of life insurance. The gentleman later developed cancer and passed away. He states:

I have never known a death to be timely…

There is no mention as to whether the dropped insurance was term insurance or permanent and no reference to his age or general health. It is a sad story for sure and one that might have ended differently had there been a little more information and discovery than just an “on paper” decision.

I can hear the conversation and it probably goes something like this …

“You have $5MM of assets [assume qualified plans, real estate, non-qualified investments], no liabilities and with your Social Security benefits and investment accounts we can generate $X in income for both you and your spouse for the rest of your lives, assuming a “safe” 4% distribution rate. Our Montecarlo analysis shows a 90+% probability that you will never run out of money, and you should be able to leave a legacy to your children and grandchildren with the remaining assets. You don’t need life insurance so let’s drop it and reinvest the premium savings into your investment portfolio or use it for lifestyle spending”.

Evan’s own words are:

As I consider my own retirement and legacy objectives (now that I am 62 and my children are in their 30s), I ask myself a lot of questions, as I am trained to do. However, many people may not think about all the scenarios, and most of them involve some level of risk outside of just the investment performance and sequence of return (Montecarlo simulation) risk. The risk of dying too soon, the risk of living too long, the risk of getting sick along the way and the inevitable risk of transfer taxes.

Consider the following questions when contemplating the use of permanent life insurance during retirement:

1. Is 4% ofyour incomegenerating assets enough for you to live the life you want to live? Could you take more income at the risk of leaving less to your children\ grandchildren?

2. If you have a legacy objective (because NOT everyone does),could you spend more and replace the inheritance with life insurance? Permanent life insurance could be your permission slip to spend more during your life while having your children receive 100% liquid cash that is income tax free and uncorrelated to any other asset class. Life insurance does not care if “the market” (any market) is down 20% the day you pass away – the value of life insurance is always 100% of what you expect it to be.

3. Could you reduce the sequence-of-return risk during retirementwith guaranteed lifetime income annuities? A life annuity will never run out of money. It is, by definition, a longevity hedge, but it will cease to pay upon your (and\or your spouse’s) death. Could you replace those annuity assets with life insurance?

4. Inwhat order are you going to spend down assets? Qualified plans and annuity assets will be taxed to your children as ordinary income when they inherit the funds. Have you considered the reality that the IRS is a 40% beneficiary of those assets? Maybe more if you have a large estate and would owe estate taxes. How does that impact the value of your legacy assets? Could you use permanent life insurance to cover the taxes on this liability or possibly allow them to convert to a Roth IRA and have the insurance proceeds pay for the taxes on the conversion?

5. Do you have any charitable intentions? You could designate a charity, or a donor advised fund (DAF), as the contingent beneficiary of your qualified plans and annuities while replacing the assets to your children with tax free life insurance.

6. How much do you like those not so cute 35-year-old children? Do THEY have kids? Do you like THEM? I’ll bet you do. How much do you want to leave them? Could you use life insurance for that?

7. Are there any special needs or disabled grandchildren? Do you want to help your children with them?

8. What if you got sick and required home healthcare or nursing home care? Is that scenario built into the Montecarlo analysis? How will an illness impact your retirement income or your legacy assets if you draw them down to pay for care? Did you know that you could add a long-term care rider to a life insurance policy? Could life insurance proceeds replenish assets expended on elder care?

9. What about life insurance cash value? How does that play into your tax planning? Did you know that cash value grows free from income taxes? Did you know that distributions from life insurance during retirement could be taken income tax free if structured properly? Did you know that you could borrow from your policies at a very low cost to no cost. Imagine having your own bank where you could borrow money for that trip to Italy.

10. Did you know that if you really needed or wanted to, you could possibly sell your life insurance for a cash payment?

I could go on and on about why permanent life insurance has a place in your portfolio during retirement but don’t take it from me. Ernst and Young conducted a very thorough study and analysis entitled Benefits of Integrating Insurance Products Into a Retirement Plan. Their conclusion was that “permanent life insurance and deferred income annuities with increasing income potential outperform investment-only approaches in our analysis.”

Mr. Beach – I am sorry. You make some good points but your article was ultimately a promotion to do a needs analysis with your firm. While I applaud your theory and agree that this should be a deliberate and thoughtful consideration, the right answer lies in asking the right questions.

Please contact AgencyONE’s Marketing Department at 301.803.7500 for more information or to discuss a case.

The start of a new year is always a good time to reflect on the past and look ahead to the future in both the near and long term. When I reflect on recent annuity performance, an old adage comes to mind: “The best time to plant a tree was 20 years ago, the second-best time is today”. That quote feels especially poignant today when looking at the sharp rise in popularity and competitiveness of fixed annuities over the last year. The best time to buy an annuity might have been last October, but the second-best time very well may be today!

What’s happening with interest rates? The expectation among many economic punditsin the coming year seems to be reflected in fixed-rate decreases at most annuity carriers. At its peak, a 5-year MYGA could be purchased at an impressive 6.15%; the same product is now available at around 5.20%. While this may seem like a large decline, these rates are still some of the highest in recent memory – higher than at the same time last year and nearly 2 percentage points greater than the same time in 2022!

Product rates and features, while slightly down from recent highs, are still historically competitive. But that is only one piece of the puzzle. Much of the market optimism is driven by individuals who are retiring now, are planning for retirement, or are in the early stages of retirement. An InvestmentNews.com article dated December 18, 2023 reports that as many as 22% of Americans and 31% of Boomers who are still working plan to retire in 2024.

Let’s not forget that annuities are primarily an insurance vehicle. How should you position product features around client objectives to meet the needs of those who are around retirement age? Following is a quick refresher on key annuity product features, where the opportunities lie, and the talking points you might employ to show how annuities can help your clients succeed in retirement.

Income Annuities

Opportunities – Consider for clients who have benefitted from market rallies and want to lock in those gains in the form of guaranteed lifetime income. An old life insurance policy with more cost basis than cash value can carry over that original basis to reduce taxable portions of income.

Talking Points – The floor of guaranteed income that annuities offer may help your clients feel comfortable investing their other assets more aggressively – a plan that may potentially improve their overall portfolio performance. These annuities offer a guaranteed income that will last as long as the client or their spouse is alive. Clients can give themselves a raise every year in retirement with an increasing income option.

Opportunities – Ideal for clients who are looking for a safe place to park funds and earn a competitive return. Changing risk tolerance? Offer an alternative that is entirely predictable.

Talking Points – Clients can park their money for 3-7 years and lock in a 5.0%+ competitive guaranteed crediting rate with tax-deferred growth and have access to funds if a need arises. The product is available for clients up to age 90 with no underwriting.

Fixed Indexed Annuities

Opportunities – Consider for clients approaching or in early retirement who do not have the same risk tolerance that they once did. Can their portfolios weather a market decline, or would they benefit from the principal protection of a 0% floor and market upside?

Talking Points – S&P 500 caps are in the 10% range, which is still twice as high as a year or two ago. Uncapped accounts offer diversification and additional upside. Income Riders provide guaranteed competitive payouts with flexibility to activate a guaranteed lifetime income stream when the client wants, while still retaining access to cash value.

Long-Term Care Annuities

Opportunities – Consider for clients who have an inforce policy with significant taxable gains. They can potentially avoid future taxes on distributions by utilizing a policy with leveraged tax-free benefits for LTC expenses.

Talking Points – Guaranteed long-term care benefits can increase as the client ages or offer an unlimited total benefit pool.

Bottom line: Over the last year, our AgencyONE 100 advisors and their clients have become more active and knowledgeable in the annuity space. If you are still not talking to your clients about annuities in 2024, someone else will be. Continue toeducate yourself about annuities so that you do not leave opportunities on the table!

Please call AgencyONE’s Annuity Department at 301.803.7500 for more information

Economic predictions abound at the end of every year. Business owners create plans and strategies for the coming year based on their own predictions and, perhaps, those of others – the experts. We continue to hear and read varied business, industry, and economic predictions, but which are correct? No one knows what will happen until it happens, but it doesn’t stop people from making predictions. Even our own Gonzalo Garcia gets caught up in the game. His ONE Idea from January mentions how much he likes reading the speculations of financial pundits. They are entertaining and sometimes someone gets lucky and gets it right. Dennis Bartos also brought us a timely piece last month about a potentially serious condition that led the US Defense Secretary to go AWOL for a few days in January and find himself in hot water because of a hospital stay. Who could have predicted that?

We hope our latest ONE Ideas have offered you guidance, inspiration, and at least one idea. With that in mind, the following is a recap of our ONE Ideas for the month of January.

Our first ONE Idea for the month is from Dennis Bartos, PA – Prostate Cancer: Forget the Defense, Let’s Go on the Offense. With Defense Secretary Lloyd Austin in the news with a diagnosis of Prostate Cancer, Dennis thought it timely to discuss the condition. His January 12th ONE Idea explored the implications of the age of onset, types of testing, scoring, and treatment, and how the AgencyONE underwriting team underwrites the condition. The ONE Idea also shares case studies from the clients of our AgencyONE 100 Advisors. This highly informative article is a must read.

The second ONE Idea for January is from Gonzalo Garcia, CLU – A 2023 Review & 2024 Predictions – Why Not? His January 23rd article mentions how little we can know about the future and how difficult it is to control its outcome. Economic predictions are everywhere and while they are often wrong, these predictions are very entertaining and get people thinking and talking. Many make their living – and quite a good one – by reading the economic “tea leaves” or their “crystal ball.” Gonzalo highlights a couple of economists in the prediction business who he likes and “make sense to him.” He goes on to overview the 2023 industry and economy and makes his own educated predictions for 2024: Interest Rates, Premium Financing, Private Financing/ Split Dollar, Annuities, M&A Activity, The Sunset, Peak 65, The Great Wealth Transfer, The National Debt, and Politics & Regulation. Stay tuned to see if Gonzalo can predict the future!

We look forward to bringing our AgencyONE 100 Advisors support, exciting content, and events in 2024 that are designed to help grow your business and post another successful year!

Remember, you can find our most recent ONE Ideas under “Updates > Blogs”on our website homepage. Additionally, a full library exists on your personal Dashboard on our website under the Sales/Marketing tab (you must have a website login for access to the complete library). If you see a ONE Idea you like, we will happily brand it for your company. Just let us know.

AgencyONE provides these ONE Ideas to help you and your clients gain a better understanding of the planning, product selection, design, and underwriting that goes into the purchase of life insurance (with and without linked benefits), annuities and disability insurance. We hope you find these ONE Ideas helpful when assisting your clients with their financial, wealth, business, and estate planning needs.

It seems that this time of year, EVERYONE has an opinion about what will happen in the coming 12 months. I “love” reading all the financial pundits speculating on how the economy will perform and which direction the stock market is going, and by how much.

I received the adjacent chart from my personal financial advisor a few days ago and it made me realize just how little we can possibly know about and control the future.

Let me start by saying that those people who are so bold as to predict the future movement of the markets (or the economy) are either arrogant, clueless, or have some other agenda. But I ask myself: “Self? How can they be so consistently wrong?”

Well, they are not always wrong … sometimes they are just lucky. Sometimes it is just better to be lucky than good.

Then there are articles like the following from John Mauldin of Mauldin Economics. Mauldin has a very tempered approach in his newsletter and I find it an interesting read, but is his crystal ball any clearer than anyone else’s? Not likely, his agenda is to sell newsletters, subscriptions, books and promote speaking engagements.

So, if most predictions can’t be counted on, why am I even taking the time to make 2024 predictions? If nothing else, entertainment value. I love these sorts of articles – they make me smile 😊.

Speaking of smiling, I recently attended a Study Group meeting in New Orleans where I had the pleasure of seeing Peter Ricchiuti, Professor of Economics at Tulane University and Founder of Burkenroad Reports. Talk about taking the prediction business to a new level! This is a very smart man, and he takes the driest of subjects, economic and financial predictions, and makes them entertaining. If you want to see a master at this, click the picture just below to watch the video:

It is as if he doesn’t take himself seriously, but he makes a lot of sense to me.

ANYWAY … 2023 was an interesting year for the insurance industry and certainly for AgencyONE. Some key highlights that emerged from 2022/2023 that will continue to create both opportunities and challenges for 2024 are:

Higher Interest Rates – This was a big part of the 2023 story and had several notable impacts:

2023 Products – We saw some meaningful increases in interest rates on some products. Of note, the John Hancock flagship product, Protection UL, had several interest rate increases for both current in force and new policies. For those of us who have been in the industry for a while, we have seen decades of nothing but declining rates on current assumption products. This was great to see, especially from carriers that benefitted existing policyholders. There were also a lot of cap and participation rate increases on the IUL side from a variety of carriers. The same can be said in the Whole Life space with dividend increases. Overall, a great benefit to most life insurance customers.

2024 Prediction – Permanent Life insurance is a great stabilizing asset, it doesn’t matter what kind (UL, VUL, IUL, WL) and LIMRA expects 2023 to end in line with what was a record sales year in 2022. IUL premium softened through the third quarter of 2023, while policy count was up, which leads me to believe that the challenges in the Premium Finance market (see below) impacted the large case IUL market. Expect to see more of that during 2024 as interest rates stabilize at a higher level for premium finance loans. Interestingly, VUL sales were up 20%, driven by a small group of carriers and I am guessing they are John Hancock, Securian, Nationwide and Lincoln, among others. This is reflective of the emergence of these carriers offering GUL products on a VUL chassis. There are other carriers developing similar products as they look to appease the independent market’s addiction to the GUL space, so expect more of that. I also expect 2024 to continue to fuel the Whole Life space as dividend rates increased pretty much across the board.

Premium Financing – Ouch!Those customers who had rate renewals on their commercially premium finance loans saw interest rate increases of double (in some cases triple) the previous year’s rate. I remember in 2021 and into 2022 seeing premium finance rates from banks in the high 2% to low 3% range. New loans in the latter part of 2023 were being offered or renewed north of 7% in many cases. This was a huge shock to customers who had large loan balances and were paying interest to the banks. Cash flowing interest payments became a huge financial strain, and many clients were NOT happy, some wanting to get out of their transactions altogether.

2024 Prediction – While there are a lot of premium finance promoters still marketing their services, I don’t see this part of the market bouncing back in 2024. I think that the combination of higher interest rates and a down year for the S&P 500 in 2022, caused a lot of ZERO’s to be credited to IUL policies. The market took a hit as consumers realized a number of things:

1. The numbers don’t always look like the spreadsheet that was sold to them;

2. That cash flow is required to service these loans; and

3. Collateral calls can and do occur if the cash value doesn’t go up as illustrated.

Private Financing\Split Dollar – In January of 2022 the 7520 rate was 1.6%, while at the end of 2023 it hit 5.8% which put pressure on the financial objectives of some transactions. For term loans, the story was not much different. The Short, Mid and Long-Term AFR rates started in January 2022 at .44%, 1.30% and 1.82% respectively, and started 2023 with massive increases and an inverted yield curve at 4.5%, 3.85% and 3.84% respectively. Rates leveled off during 2023 and the yield curves flattened relatively but now show a bit of a “U” at 5.26%, 4.82% and 5.03% respectively. This also had an impact on transactions that use the Federal AFR rates such as GRATS, CRATS and other discounting strategies.

2024 Prediction – I have always said that I would rather pay myself or my family interest (such as in a private financing transaction) than pay it to a commercial bank. IRS-published rates are more attractive than commercial lending and for those who have the assets to do a private financing transaction, this may replace some of the lost premium from premium financing in the estate and wealth transfer market. I am also a big fan of Split Dollar, and we are seeing more and more of it as a tried-and-true strategy for estate planning and executive compensation. Finally, private financing transactions between the older generation and younger generation(s) are very attractive at many levels. I expect to see more and more interest in this space.

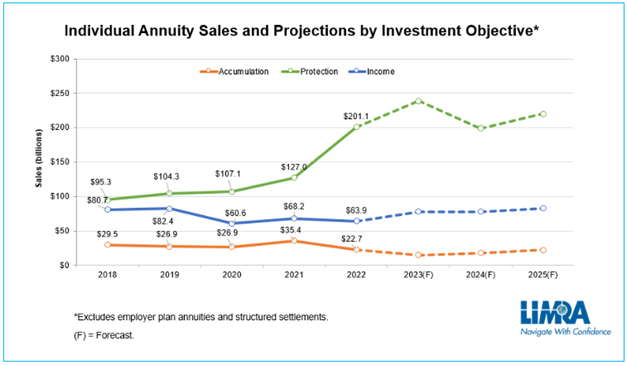

Annuities – If nothing else, this was the most meaningful market impacted by rising interest rates with sales shattering the 2022 record of $313 Billion. While final numbers are not yet reported, LIMRA was predicting over $350 Billion for 2023 and some experts are predicting another record year in 2024. I believe the experts, so I don’t expect the annuity rocket to slow down any time soon. There are other reasons discussed below that also play into this. If you are not offering your clients fixed-rate annuities, someone else will be, so don’t ignore this space.

M&A Activity – As the cost of capital rose, deals got more expensive for buyers and the market cooled with insurance brokerages as multiples came off their peak. M&A activity dropped by 17% according to Marsh, Berry & Co, LLC during 2023. Not much to say here, but as interest rate increases have subsided and the insurance industry has gotten a year older, many practitioners in both the retail and wholesale insurance business are looking to sell before the dry powder runs out in the Private Equity space.

The Sunset is coming, The Sunset is coming – As AgencyONE and many others in the industry have talked and written about, the Sunset Provision of the Tax Cut and Jobs Act of 2017 will take effect on January 1, 2026 – two short years from now. There has been heightened awareness of this amongst the legal, accounting, and financial services professionals during 2023, but clients still seem a bit non-plussed. People with a net worth of over the current gift and estate exemptions, which sits at $13.61MM for individuals ($27.22MM for married couples) in 2024, would be well served to begin taking advantage of the “gift” provided them by TCJA to transfer assets to younger generations during their life or to plan their estates to optimize wealth transfer during the next two years. You don’t have to be in that financial stratosphere, however. High net worth individuals with high incomes and many years left of compounding estates will be well served to do an estate projection and act before the end of 2025. Attorneys will be hammered and generally not as accessible as we get closer to that sunset. Additionally, expect higher income tax rates as well, as we revert to a maximum tax rate of 39.6% versus the current 37%.

2024 Prediction – This year and next will be very busy for those practitioners who call themselves estate and gift tax planning experts. Motivating consumers to see this for what it is, a massive tax planning gift that could benefit the next generation(s), will be the most important activity we can engage in. Income tax planning will also be critical and well-designed life insurance, as a tax-free bucket (either during life or at death), is an excellent tool in the toolbox.

Peak 65 – We have been saying for years that 10,000 Americans turn age 65 every day. Well, this year is different. That 10,000 number will increase to 12,000 in 2024. 4.4MM people will turn 65 in 2024. The impact of the aging boomers is extraordinary in so many ways, but the peak of the aging of America is occurring THIS YEAR! Think of the opportunities for longevity planning with guaranteed income annuities, for generational wealth transfer planning (which is further highlighted by the previously discussed Sunsetting of the TCJA), Long Term Care needs, business owner exit planning needs … I could go on and on.

2024 Prediction – I am so bullish on finding ways to advise aging Americans and there are so many needs that are largely unadvised and unfulfilled. I believe that the aging of America is going to hit us hard this year and offer financial security professionals a massive opportunity to help consumers in ways we never thought possible, specifically around longevity hedging with income annuities and morbidity hedging with some form of Long-Term Care solution.

The Great Wealth Transfer – Do you know what happens when the largest generation in the history of mankind (The Boomers) fall in love and start to multiply? Generation Y, affectionately known as Millennials, happens. The Boomers have also created the largest amount of wealth in history. This Millennial generation is now larger than the Boomers, as some Boomers have begun to pass away, and they are going to be the beneficiaries of the largest wealth transfer ever in the next 20-30 years. While Millennials seem face down into their phones or tablets for everything, study after study shows that they want and need advice from a real person.

2024 Prediction – This is a massive opportunity, but we must meet them where they are when delivering financial guidance. They know a LOT more than their parents (the Boomers) did at their age because of the way they consume information and you had better be prepared for that if you are advising this market segment. The amount of wealth they are going to inherit is staggering and we must help them plan their own financial lives and prepare them to be good stewards of this extraordinary gift.

Global Unrest – We now have two very visible wars going on in the world and there are many smaller skirmishes that nobody even talks about. The risk of continued war and unrest is high, and it puts a tremendous amount of pressure on the American people to support democracy around the world. Of course, this comes at a cost. I have no predictions on war other than to move on to my next point, which is …

The National Debt – Yes, we will continue to be the bullhorn for democracy around the world and we will continue to send money to Ukraine and Israel and other less significant but important democratic countries, but how do we continue to pay for this generosity? At 33+ trillion dollars of debt, interest rates up and a Congress that cannot get anything done, we are headed for a train wreck, or at a minimum, a higher tax environment.

2024 Prediction – Who knows? But, as a country, we are burdening our children, grandchildren and great-grandchildren with some very dire economic realities or staring down the barrel at a massive revenue generation effort by the Federal Government – otherwise known as higher taxes. We just cannot continue to move in this direction. That said, the insurance industry has one of the most favorable tax solutions at our disposal if Congress does not take it away. This tool, life insurance, also serves to create and provide liquidity with very favorable tax treatment. We need to continue educating consumers and look for new ways to distribute our products, solutions, and services. I see continued change in insurance distribution with more and more players and technology vying to get into our space.

Politics and Regulation – Yes, it is an election year and even the best prognosticators don’t know what is going to happen. I have no predictions and even if I had an opinion, this would not be the place to voice it. The bottom line – there will be a lot of continued divisiveness in politics regardless of the outcome of the election…and with that comes political agendas. More taxes, less taxes, more regulation, less regulation. Right now, all the noise is about the Department of Labor Fiduciary Rule and like our Congress, the divisiveness on this issue is enormous. Calling how we get paid to advise clients and other advisors on financial security should not be referred to as “junk fees”. As I have discussed before, the conversation should not be about commissions versus fees. It should be about acting in the best interest of the client and making appropriate recommendations for risk management and protection products AND providing diligent ongoing reviews and customer service. We have a big battle ahead of us on this one. Also, we need to keep an eye on the Long-Term Care mandates currently being reviewed in any number of states, California being the biggest. We don’t want a repeat of what happened in Washington.

2024 Prediction – I am not bold or arrogant enough to predict anything here, but I will conclude with this … If you look at all my previous points, you will notice that it is a VUCA world (Volatile, Uncertain, Complex and Ambiguous) and we must recognize that reality in order to better guide our clients on the crazy journey called life. Making predictions as to where the market is going and what is going to happen to the economy, or in our politics, is a fool’s errand. More and more, in a post-pandemic era, we are recognizing the possible value of the lessons that Mother Nature taught us and continues to teach us.

I truly believe that the opportunities ahead of the financial security profession are endless and we are at a point in history, demographically, economically, technologically, politically, and otherwise, where the VUCA-ness of life is overwhelming to our customers. The sooner we recognize this and empathize with that reality, the better financial guides\coaches we will be to them. Only then will we be able to be true fiduciaries.

I want to thank everyone who was a part of AgencyONE’s journey during 2023 and encourage those of you whom we have the honor of serving (and all financial professionals) to recognize that your clients need your sage wisdom and guidance – today more than ever.

With the Defense Secretary, Lloyd Austin, going AWOL recently with a newly diagnosed Prostate Cancer, it seems an appropriate time to visit the topic – Prostate Cancer, PSA readings and the life insurance underwriting concerns surrounding elevated PSA’s.

Prostate Cancer is the third leading cause of cancer deaths in men in the US. However, the very good news is that despite a prostate cancer diagnosis, only about 1 in 40 (very low risk) will actually die of the disease. What that means is that routine PSA testing is working and we are finding these cancers early. Yes, men should get PSA/ Free PSA routine testing.

This week’s ONE Idea will discuss things to consider when presented with a client who has had prostate issues.

AGE OF ONSET

Nearly every man over the age of 90 (almost 100%) will have prostate cancer present when they die, according to autopsy statistics. However, men are more likely to die WITH the cancer present than die OF the disease! This statistic shifts dramatically the younger we areand is in direct correlation with the levels of testosterone present at younger ages and diminishes as men get older. Testosterone is like Miracle-Gro to a prostate cancer cell so with testosterone levels falling off with age, the prostate cancer tumor cells grow much more slowly. Conversely, at younger ages with higher levels of testosterone, real mortality risk is present.

PSA

The PSA blood test (Prostate Specific Antigen) has been utilized effectively for decades as the best screening test to detect prostate cancer. Most men under age 70, will have PSA levels less than 3 but even up to 4 is considered normal. The ABNORMAL flag arises when PSA numbers are above 4.0. Every male above age 50 should have PSA and Free PSA testing performed at the same time as routine blood testing for comparison purposes moving forward.

FREE PSA

This blood test is often performed in tandem with the basic PSA screen. Free PSA breaks the total PSA into two component parts like total cholesterol testing that is broken into good (HDL) and bad (LDL) cholesterol percentages. The Free PSA component for a normal healthy male is 25%. Flags of concern don’t start until that number drops to 18%. So, the lower the Free PSA component, the more likely that a prostate cancer exists.

PSA VELOCITY

This term applies to the rise in PSA levels that routinely occurs as men get older and the prostate naturally enlarges (BPH-Benign Prostatic Hypertrophy). For ease of understanding, let’s say a male 60 has a PSA reading of 2.0 while the next year, the PSA reading is 2.5. A flag should be raised by a competent physician that, although the PSA level is still in the normal range below 4.0 as discussed earlier, this PSA velocity (speed of rise) year-over-year is a concern and should be investigated. In this example, the PSA velocity is 25% and a flag should be raised. That is exactly what happened in a case AgencyONE had last year with a very astute urologist in Pittsburgh.

THE DRE

The dreaded Digital Rectal Exam – a gloved finger examination of the prostate via the rectum. The prostate should be smooth and firm but in prostate cancer, nodules may be present, or the gland can feel boggy and enlarged. An abnormal DRE warrants further investigation by the doctor.

THE PROSTATE BIOPSY

If an elevation in PSA exists and the physician further screens with Free PSA testing or other diagnostic tests available today (like MRI), the next step could be a biopsy. The prostate gland is like a plum or apricot in size with two “lobes” and the urethra running through it. When/if the prostate enlarges, it can impinge on the urine flow through the gland (another topic for another time). In the case of a Prostate Biopsy, it is normal procedure to take 6 samples from each side of the prostate gland so 12 samples total from targeted and documented areas of the gland. These are called CORE SAMPLES and result in a pathology report for all 12 of these prostatic tissue samples.

GLEASON SCORE

The biopsy cells are graded on a scale of 1 to 5 as there are 5 very distinct cell patterns that occur as normal prostate cell tissue changes into tumor cells. The first score involves the predominant pattern of cells in the biopsy specimen. The scoring then takes a second step noting the second most prominent pattern and adds them together resulting in the TOTAL GLEASON SCORE. So, a male with a biopsy grade of 3 might have a SECOND most predominant pattern of 4 making a total Gleason score of 7 (3+4=7). A Score of 7 is a serious cancer. A score of 6 is less serious and more common. Higher numbers are worse.

TREATMENT OPTIONS

Prostatectomy – the surgical removal of the prostate does result in a second pathology report since the first report of Gleason Scoring was the result of just 12 biopsy probes. The Gleason Score on the final whole gland pathology can change for the worse.

Brachytherapy – Radioactive seed implants result in destruction of prostate cells from the inside out and have much less complications than the results of a total prostatectomy.

External beam radiation – Improved and better-focused medical technologies have created less complications with this course of therapy.

Active Surveillance – also called Watchful Waiting. This treatment option is noteworthy because a younger male, say age 60, with a low Gleason Score prostate biopsy might opt for no treatment since prostate cancers are slow growing and watching the PSA velocity may be the best course for a couple years. Additionally, there can be serious life changing complications with the treatment of prostate cancer, such as male erectile dysfunction. The second group of males – age 70 and over – seems to be the statistical cutoff line (the Defense Secretary is 70). Again, testosterone levels are falling so the cancer does not grow as fast and clients are likely to die with prostate cancer, not of it.

Underwriting a Watchful Waiting case can be challenging as many carriers prefer NOT to participate unless a definitive treatment has been chosen.

Case examples:

1. Mr. Smith, age 58, had an annual checkup 3 years ago. A lab panel was completely normal and included a PSA reading of 2.8. However, the attending physician APS notes indicated concern about his previous PSA reading of just 2.15. This .75 rise (PSA VELOCITY RATE) in Mr. Smith’s PSA reading warrants further investigation. The subsequent workup found a significant 4-core sample prostate cancer graded Gleason 7 (3+4). The client elected for removal of his prostate. No further spread was noted beyond the gland. AgencyONE was successful in negotiating a Standard Plus offer, and $4 million of permanent life insurance protection was placed for Mr. Smith.

2. Mr. Johnson is 64 years old and received a fresh diagnosis of Gleason 6 (3+3) Prostate Cancer in 2022. The client chose Watchful Waiting (active surveillance) which calls for follow-up biopsy checks, sometimes annually. In this case, Mr. Johnson underwent a one-year follow-up biopsy in December 2023 which showed a similar Gleason Scoring and no significant increase in spread inside the gland (core sample percentages). AgencyONE negotiated and received a STANDARD offer. The case is being finalized now at $7.5 million face.

AgencyONE’s breadth and depth of medical and underwriting knowledge and experience is a tremendous benefit to all of our advisors and their clients. We look forward to helping you with your 2024 cases and beyond.

Please contact AgencyONE’s Underwriting Department at 301-803-7500 for more information or to discuss a case.

As 2023 comes to an end, we begin to reflect on the year and find that reviewing our ONE Ideas helps us evaluate the last 365 days. Our ONE Ideas – an important part of our communication with our AgencyONE 100 Advisors – help to convey what is happening in the industry and what is on the mind of our Advisors and their clients. 2023 was an eventful year and presented interesting advanced planning concepts, case design scenarios, and underwriting case studies. We are pleased to provide this annual review and hope that it offers you some insight, answers, and/or ideas for your existing or future cases. Any of the following ONE Ideas may be customized for the business and/or clients of our AgencyONE 100 advisors.

This ONE Idea will be our final publication of 2023 as we look forward to next year and the growth and opportunity that 2024 holds.

In this article, Gonzalo Garcia, CLU reflected on the industry in 2022 and what he expected to see in 2023. He discussed his concerns in both the carrier/manufacturer and distribution sides of the business and what that could mean for our industry moving forward. Interest rates continued to affect carrier product line-ups and the direction many of their businesses have taken. Changes in distribution geared up and many M&As and consolidations happened (including ours).

This ONE Idea focuses on how taking advantage of trusts and funding them with properly designed Life Insurance can assist with estate planning for your high-net-worth clients and minimize taxes given the potential sunset of the TCJA.

This ONE Idea provided a review of the Annual Conference held at the Dupont Circle Hotel in Washington, DC from April 30 to May 2, with a bonus session on May 3 which focused on working collaboratively and how to get more referrals from Centers of Influence (COI). The annual meeting welcomed existing and new advisors to our largest Annual Conference to date! Attendees heard from leading speakers and industry experts discussing topics important to advisors, their clients, and their business. At the bonus session – High Performance Collaborative Teams (HPCT) – AgencyONE 100 insurance advisors attended with COIs that they had invited (legal, wealth, estate, accounting) for a collaborative meeting that centered around a detailed and evolving case study. The ultimate goal was to create a financial plan that considered the expertise from each of the planning specialties and was customized to the unique needs of the client. This ONE Idea also provides links to all the speaker meeting presentations that we were authorized to share! Save the Date for our 2024 Annual Advisor Conference on April 28-30 at the Dupont Circle Hotel in Washington, DC. We hope to see you there!

In this article Gonzalo focuses on the opportunities available to advisors who understand where the Gaps in the Financial Service industry exist in the minds of the customer. For example, 82% of customers expect their Financial Advisors to offer Life Insurance Advice while only 12% actually do! Gonzalo goes on to list the areas of demand in the marketplace that are NOT being fully met that offer REAL opportunities to financial advisors. He also discusses the importance of professional collaboration with other Centers of Influence involved in your clients’ financial, wealth, and estate planning. Well-timed and knowledgeable collaboration will provide your clients with a more “well-rounded” financial plan and ultimately help to build your business. Our High Performance Collaborative Teams training focuses on developing and nurturing these relationships with your Centers of Influence to help generate more referrals.

Gonzalo was inspired to write this ONE Idea as a result of a Motley Fool article he read that discussed Roth IRAs and why investors should consider them. While Roths may be the right solution for some, Gonzalo points out that Roths have limited applications for many and, even if someone DOES qualify, contribution amounts have strict limits. Additionally, Gonzalo notes that the Motley Fool article does not include an IMPORTANT and viable alternative for investors who do NOT qualify for a Roth – a Variable Life Insurance solution. Gonzalo dives into the specifics about how a well-designed Variable Life policy offers the same benefits, possibly better, than a Roth IRA [doesn’t have Modified Adjusted Gross Income (MAGI) or contribution limits and offers real tax benefits].

This ONE Idea explores Premium Financing and its popularity with our AgencyONE 100 Advisors. Most have considered the planning strategy for their clients at one time or another. While some transactions have resulted in considerable angst for both advisors and clients, these arrangements can still be attractive in the right situation. Inforce premium financed policies SHOULD be reviewed periodically to make sure that the long-term objectives of the policy owner are still being met. Due to changes in the economy, many existing premium-financed policyholders have come up against serious hurdles. If you have a client who has called to discuss a problematic life insurance premium financing transaction, AgencyONE may have a solution.

Gonzalo has been talking about this for quite some time and it is on the mind of many other planning experts as the sunset date approaches. In this ONE Idea, Gonzalo reviews some exemption history, discusses the current predictions, and explores excellent planning options for you and your clients to consider that include life insurance in preparation for the upcoming changes.

Gonzalo’s commentary applauds the firms that are working hard to develop and embrace technology that is changing the dynamics of the life insurance industry. He focuses, however, on the importance and irreplaceability of human interaction and expertise that is required for the many cases that do not fit neatly into a box. A professional human “touch” remains critical to the specialized handling and strategic placement of your cases.

Holistic financial planning is far more extensive than just creating a financial plan and providing investment advice – a concept Gonzalo has been talking about for many years. In this article, Gonzalo discusses how, individually, an advisor can successfully meet many of their clients’ expectations, but to provide a thorough and fully integrated plan for financial wellbeing, it takes a team of professionals to meet the needs of the client and the family.

This ONE Idea summarizes the importance of making policy reviews a part of your planning practice with your clients. They help you nurture client relationships, build trust, and keep you abreast of changes in their lives and financial situation. This ONE Idea discussed carrier product information to use during policy reviews with your clients who have Term policies.

In this article, Ed Stark, CLU, ChFC, RICP offered a refresher on current product availability and new opportunities that brought success for our AgencyONE 100 Advisors and their clients. Ed outlined the specific products and the steps AgencyONE took to help the advisor achieve the financial planning goals of the client.

This article by Ed Stark discusses the importance of policy servicing and the opportunities it offers the client and the advisor. It talks about a review that revealed a policy that no longer served the client but presented an opportunity for a unique case design specifically designed for the client.

In this ONE Idea Ed Stark discusses the resources and platforms AgencyONE uses to provide our advisors with the necessary comparisons for their client’s cases. Our most popular comparison platforms are the iPipeline Term Quote Engine, Winflex, Ensight, and InsMark. These important tools help AgencyONE accommodate case design requests and comparisons and are capable of providing simple or very advanced marketing strategies depending on the client’s financial needs.

This ONE Idea summarizes how cash value life insurance can offer your clients the benefits of tax-free income and provide another income source in addition to those they currently have in place. The article looks at a design that features multiple insurance solutions and includes sample reports and comparisons detailing equity accounts versus insurance accounts. This ONE Idea is a great one to share with your clients who have ample investments and don’t fully recognize the varied benefits of life insurance.

Adding value to the insurance plans you offer your clients must be a priority if you are to build trust with your clients and set yourself apart from your competitors. In this ONE Idea, Ed discusses options to consider for adding value to your clients’ policies and your business.

This ONE Idea from Dennis Bartos, PA explored a powerful underwriting opportunity and our selection as a pilot site for testing a NEW DIRECT UNDERWRITING program. We had success with several of our AgencyONE 100 advisors’ large cases which were granted improved underwriting. We continue to see this as an opportunity to position cases that might otherwise have been unfavorably rated or possibly declined.

This article discusses the importance that hydration plays in maintaining our body’s health and how it can affect lab results and ultimately underwriting. In this ONE Idea, AgencyONE’s underwriters delve into the impact that exercise can have on an insurance exam. AgencyONE underwriters emphasize the IMPORTANCE of educating your clients. We have one-pagers and videos that can assist in making sure your clients are ready for the insurance exams they may be required to take.

One (1) out of every seven (7) strokes are attributed to undiagnosed and/or untreated atrial fibrillation. Known as AFib, it is the most common kind of heart arrhythmia in the world. In this ONE Idea, underwriters Dennis Bartos and Julie Melendez discuss the definition, causes, and symptoms of atrial fibrillation, along with existing and newer treatments that have recently become available. It also outlines what underwriters look for when evaluating a case that presents with AFib and an actual AgencyONE case study that demonstrates how important preliminary underwriting and advisor involvement are to the successful outcome of a case.

In this ONE Idea, Dennis outlines the options for those clients who have inforce policies that no longer fit their needs or could be improved upon. Some of these policies are no longer performing as originally designed. Some clients have term policies coming to an end and need to be converted to permanent coverage. Some clients have health issues that have improved and may be eligible for a rating reduction, while others may not need coverage any longer and are candidates for life settlement. There are as many options as there are types of clients.

While Medical Underwriting is the primary focus in most of the cases at AgencyONE, cases with a focus on Financial Underwriting are increasing. In this ONE Idea, Dennis discusses and defines the criteria that must be considered for financial underwriting.

While this ONE Idea humorously refers to a Huey Lewis tune from the 80s, Dennis’ article and the case study address the impact that the new weight loss drugs like Ozempic have had on the health and life insurance underwriting of those prescribed and using these drugs.

The amount in this title represents the value that is currently held inside deferred annuities. This article by Craig Baumgarter, RICP discusses the opportunities that are available for your clients with existing annuities that may be expensive and variable, indexed with a guaranteed minimum crediting rate, or fixed and not competitive in today’s market.

This article penned by Craig discusses the important benefits of Qualified Longevity Annuity Contracts (QLACs). This annuity product helps to create a lifetime income for your clients who may be afraid of outliving their money and reduces your clients’ taxes by repositioning funds from highly valued Qualified Accounts with increasing annual Required Minimum Distributions (RMDs).

Craig explores how to create a retirement income plan for your clients who have relatively conservative risk tolerances. He discusses the time-tested solution of laddering bonds and then considers a more efficient solution including a comparative case study using an Annuity that does not introduce excess risk.

In this article, Craig shows the progression of a case and optionality when the goal is for both death benefit and living benefits coverage BUT the client’s budget is driving the case. The Case Design team and advisor considered initial options which were great choices but turned out to be too expensive for the client who had two children still in college. Ultimately, the client agreed to an excellent and affordable solution that locked in insurability for a future policy conversion tailored to the client’s needs!

We wish you and yours a happy, healthy, and safe holiday season and a New Year full of blessings, possibility, and prosperity!

AgencyONE looks forward to providing more terrific content in 2024.

Please contact our Marketing Department at 301.803.7500 for more information or to discuss a case.

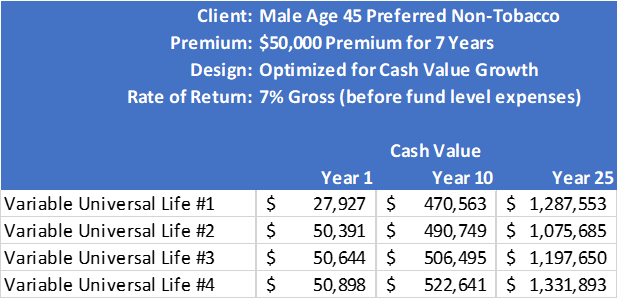

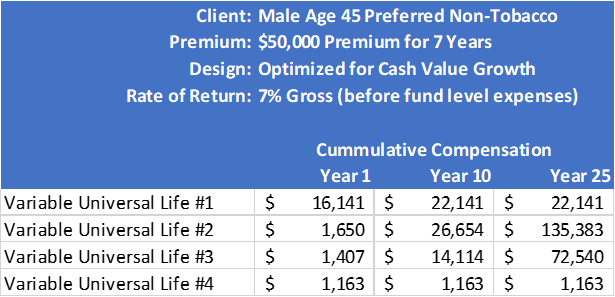

I am probably going to catch a LOT of grief for this article, but frankly, I really don’t care. I am trying to look at the numbers as impartially as I can and would welcome a math lesson if I have this wrong.

For the record, I am a BIG fan of a No-Load Variable Life solution that came to market over a year ago offered by a well-known insurance company. In fact, I like this product so much that I bought a policy for both my wife and myself and rolled some older fixed account cash value contracts into this policy via a 1035 exchange. I have been funding it regularly and understand how life insurance works better than most people. I have been in this business for 40 years and I do not need an advisor to either “sell me” or “advise me” on it – a big difference versus a consumer to whom we owe a fiduciary duty.

Bear with me because there are a lot of numbers and comparisons between a fully loaded, registered representative (FINRA) sold Variable Universal Life product and a No-Load\AUM fee-based life product from the same insurance company. My analysis will focus ONLY on life insurance and will not include annuities.

Let’s begin with a question. Which of these four life insurance products would you recommend if you thought ONLY of your client’s best interest? Remember, these products are all from the same highly rated mutual company, same underwriting class, same policy construction, etc. Please don’t say that you would not recommend any of them, you must pick one – play the game.

If I had to make a choice, I would recommend Scenario #4, all things being equal. It has more first year cash surrender value (in fact it is higher than the first-year premium) AND has more long-term cash value growth than the others over both 10 and 25 years. Full stop, it is the best solution for the client or in the client’s best interest. Right?

But all things are not equal.

Same products, same question. Now which one would you recommend to your client?

Tougher question is it not? Now you must think about your own livelihood, your firm’s profitability and the value of your time and advice unless you charge fees that are NOT related to Assets Under Management, such as flat or hourly fees. You are in the service business, and you are constantly valuing your time and expertise. After all, you are in this profession to make an honest living, right?

So, let’s unpack this.

Scenario #1, as you can imagine, is a fully loaded, “high commission” solution.

Scenario #2 is a low load, advisory solution where the advisor charges a 1% fee on the AUM, which is the cash value of the policy.

Scenario #3 is the same low load, advisory solution where the advisor charges a .50% fee on the AUM.

Scenario #4 is also the same low load, advisory solution that pays a one-time concession to a Broker Dealer for registering the account (it is a security, after all) and to a registered representative\insurance agent for completing the application, facilitating the underwriting for the insurance, and servicing the account. You, as an advisor, do not collect anything unless you are part of that process or, of course, unless you charge a non-AUM related fee to your client.

A fair set of questions would have been if I had eliminated Scenario #4 and didn’t ask you to work for free. You don’t work for free, do you? I will bet that you charge an AUM fee that is somewhere between .50% and 1% (possibly more for lower size account clients).

If that is the case, then the compensation expense of an insurance contract is always more expensive over the life of the contract in an AUM model than in a front end loaded, commission-based model. In fact, it is a LOT more expensive and is reflected in the cash value of the policy. The cash value of Scenario #2 – the 1% solution is over $200,000 lower over a 25-year period. What if the clients lived to the age of 90 and we are looking at 45 years? The answer is that the cash value difference would be close to $2,000,000 lower. That is the magic of compounding but also the dirty little secret of the AUM based model.

[In the spirit of full disclosure, for all scenarios I used the actual fund expense fee of the S&P 500 Index fund available in the underlying fund options. Scenario #1 has a .26% fund level fee, while scenarios #2, #3 and #4 have a .18% fund level fee. If I could run an apples-to-apples comparison, the differences would be even greater!]

So which solution is “in the client’s best interest”? Fully front end loaded commission or low load with an advisor-based fee model? There really is no right answer and it goes back to the suitability issue of client time horizon.

I can remember when I was obtaining my securities licenses back in the mid-90’s and mutual funds had A, B and C shares. I had to get broker-dealer approval to sell C shares and “paper the file” because it was ALWAYS more expensive over the long term for the consumer to pay a lower front-end load with a trail fee (C-Shares). Life insurance is a long-term solution, but it needs to be managed, just like any other portfolio (IRA, 401K, Managed Non-Qualified Portfolio, etc.).

I would also like to make the comment that a well-managed and well-designed VUL solution by an investment advisor should substantially outperform one that is not managed, as so many are. Advisor Alpha is what many call this and what the advisor is being paid for via their commission or AUM fee. I will quote a Vice President from a well-known insurance company who told me that 60% of all subaccount values on a particular Variable Life product that they offer are sitting in the Money Market or Fixed account. This is unconscionable! It is also not dependent on how the advisor gets paid, because a fully front-end loaded solution could be equally serviced and managed. I have been doing this long enough to know that, at the end of the day, many agent\registered rep initiated variable life sales don’t fail because of the commission versus fee conversation. They failed because the agent\registered rep did not manage the account as they should have. They did not monitor the policy, make portfolio adjustments and rebalance accounts, which is part of the value or the “fiduciary duty” that the advisor owes the client, and that the client is paying for.

Merriam Webster explains in their definition of fiduciary the following:

Fiduciary relationships are often of the financial variety, but the word fiduciary does not, in and of itself, suggest pecuniary (“money-related”) matters. Rather, fiduciary applies to any situation in which one person justifiably places confidence and trust in someone else and seeks that person’s help or advice in some matter. The attorney-client relationship is a fiduciary one, for example, because the client trusts the attorney to act in the best interest of the client at all times. Fiduciary can also be used as a noun referring to the person who acts in a fiduciary capacity, and fiduciarily or fiducially can be called upon if you are in need of an adverb. The words are all faithful to their origin: Latin fīdere, which means “to trust.”

Let me repeat the most important phrase – “fiduciary applies to any situation in which one person justifiably places confidence and trust in someone else and seeks that person’s help or advice in some matter”. It does not contemplate how that person gets paid, but it does put financial advisors in a position to act in the best interest of the client at all times, as the definition suggests.

Assuming we are doing our jobs to the best of our ability and in the best interest of the clients, let’s stop bickering about how we get paid and let’s start taking care of clients. OH, and let’s focus our regulatory efforts on training and character building because there are a lot of unscrupulous people in our profession. I have seen them on the insurance side and on the investment banking side, having been part of both worlds during my career.

I thought that this was a timely discussion as the insurance industry gears up to do battle with the Department of Labor on their third attempt at best interest\fiduciary legislation.

Please contact AgencyONE’s Marketing Department at 301.803.7500 for

Every morning I read financial journals and various news publications to keep abreast of what is happening in the financial services industry, and regardless of the day of week or publication I review, the concept of “holistic wealth management” or “holistic financial planning” continues to emerge as a major subject of discussion.

A recent white paper from SS&C, a technology and investment operations company and, developers of the Black Diamond Wealth Platform, grabbed my attention. It opens with the following statement:

The wealth manager’s role is evolving, driven by changing client expectations and new business realities. Clients want to have a complete picture of their financial life beyond their investment portfolios so they can make important life decisions. They seek professional guidance to put all the pieces together, particularly for the complexities associated with taxes, retirement income, property ownership, estate planning, and more. At the same time, advisors are looking to provide broader services. Their traditional investment management offering is becoming commoditized, which means they need new ways to differentiate themselves and deliver client value. As a result of these converging interests, the trend toward comprehensive or “holistic” wealth management is accelerating.

While the white paper is fundamentally a pitch for their technology platform as well as their relationship with DPL’s Advent Insurance Marketplace (a fee-only annuity and life platform), it does make many excellent points, which support what I have been saying for years. The bottom line is that holistic financial planning is far more extensive than just creating a financial plan and providing investment management. In fact, the day will come soon enough when even the commoditization of these services will not matter, as the opening statement suggests, because Artificial Intelligence will likely replace our role in many of these sorts of tasks. But will it 100% replace the advisor? I do not see that happening.

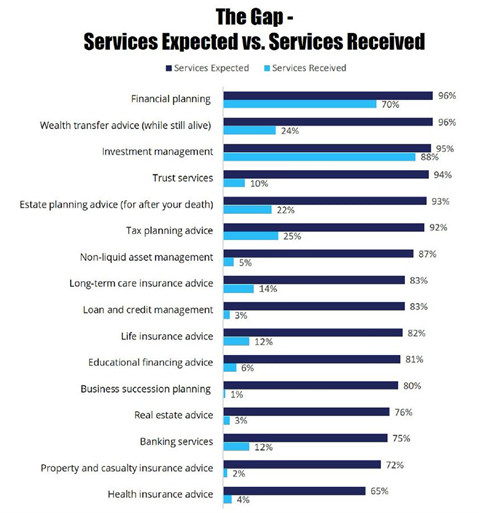

Remember this chart below from the Spectrem Group study from 2021? It has been floating around and referenced all over the press and social media since then. I wrote about it back in May of 2022.

Holistic, to me, absolutely means providing financial planning and investment management services. BUT what about all of the other services that clients expect that are not being provided?

Was this study the impetus for a more robust conversation about “holistic wealth management”? Was it a wake-up call for the Financial Planning community to broaden their perspective with respect to the financial wellness of the people they serve?

In early December 2023, The CFP Board Center for Financial Planning hosted the Academic Research Colloquium for Financial Planning in Arlington, VA – my hometown.

Dr. Sonya Lutter, Ph.D., CFP, LMFT, Professor of Practice, Director of Financial Health and Wellness, Texas Tech University, was to deliver the keynote presentation “based on her research into the relationship between the psychology of financial planning and a holistic planning process that includes risk management as well as wealth accumulation and client outcomes” according to the event’s website. I find it fascinating that holistic planning is being talked about at an event like this (an academic research colloquium) and I applaud this wholeheartedly.

An attendee/friend at the conference told me that the research distinguishes between financial stress (the feelings caused by specific stressors) and financial anxiety which is a negative state not specifically related to an identifiable source. “Advisors are effective in reducing financial stress, but financial anxiety is more the domain of therapists”, he quoted Dr. Lutter.

Are financial planners being asked to be therapists now? I did not see that service on the list expected of our profession in the Spectrem Study referenced above.

As a point of emphasis, it is not reasonable to expect that an advisor could deliver all the services noted in the above chart. It would be like asking an internal medicine doctor to treat a patient for cancer and cardiac disease among other ailments. It is just not possible – they don’t have the training for it. There are other specialists that can collaborate for a better health outcome for the patient.

A CFP Professional completing a financial plan or offering investment advice would not draft a trust document or file tax forms unless they were licensed to do so as an attorney or CPA. Furthermore, they may not recommend life or health insurance if they are not licensed to do so or otherwise not knowledgeable in the area. For the same reason, they would also not provide financial anxiety therapy to clients without a certain amount of expertise or licensure. There is, in fact, a whole emerging field in behavioral finance, which is fascinating.

Providing holistic guidance and creating financial and overall general well-being should be done by a team of professionals who can truly collaborate for the benefit of the client and their family. This team of people should be able to provide a diverse skillset, expertise, care, and a desire to serve as part of a collaborative advisory group.

Whether you are an attorney, a CPA, a Financial Planner, a wellness therapist, or an insurance specialist, finding the right team of professionals to better serve the diverse needs of your clients is critical to their long-term financial well-being and will go a long way to meeting the very expectations that they have of us.

As a final note, my friend also reported back to me that one of the conclusions from a different academic presentation at the CFP Board Center for Financial Planning was that “research says that the value of holistic, personalized advice regardless of fee or commissions is the equivalent of an 82% increase in income”. Presumably for the client, NOT the advisor. And, if a representative and keynote speaker for the CFP Board said it, it must be true, right?

As we sit here today and try to figure out the implications of the proposed Department of Labor Fiduciary Rule 3.0 ruling on this whole issue, how an advisor chooses to get paid for his or her services does not appear to be the issue to successful financial outcomes of our clients. This is a discussion for another day, as the Department of Labor Hearings have just occurred (December 12 through December 13, 2023), on its proposed “Retirement Security Rule: Definition of an Investment Advice Fiduciary.”

Please contact AgencyONE’s Marketing Department at 301.803.7500 for more information or to discuss a case.

As an advisor, you always look for ways to add value to the insurance plans you recommend to your clients. One example is to suggest a LTC/Chronic benefit rider on their life policy. Riders have become very popular in recent years. According to LIMRA’s 2022 Insurance Barometer study, “4 in 10 consumers are very concerned about how they will pay for long-term care services”. Many of the case designs we run for our AgencyONE 100 Advisors include these riders. They offer clients another layer of protection by covering future long-term care needs. Consider pricing your cases with AND without these riders to see if the cost is justified, but…. which product solutions work best with an LTC/Chronic Benefit Rider?

Let’s look at two case scenarios – the first using an Accumulation-focused solution and the second a Protection-focused solution.

Accumulation Solutions

Let’s assume a 52-year-old male with a Preferred NT rating and a $25,000 annual premium payable to age 65. The initial death benefit is $328,207. The rate of return (ROR) is 6%, and the policy will pay income from ages 71-85. A properly designed accumulation solution will usually have a minimum non-mec death benefit based on the premium contributed. The death benefit increases according to the cash value until the premiums stop and the death benefit drops to corridor, which maximizes cash values and minimizes charges. Adding a Long-Term Care (LTC)/Chronic Rider may lower the initial minimum non-mec death benefit slightly, but the real impact on the policy occurs later during the cash accumulation and income phase. The addition of the LTC Rider sets the monthly benefit to the initial face amount.

Accumulation Policy Values Without an LTC Rider

The projected accumulation value on the initial death benefit ($328,207) is $426,398 at age 65. The projected income using withdrawals to basis and then standard loans will be $55,080 per year from ages 71-85.

Accumulation Policy Values With an LTC Rider ($6,466 monthly benefit for 50 months)

The initial death benefit is $323,301 (approx. 1.5% [$4906] less than the initial Death Benefit without an LTC rider) with a projected accumulation value of $418,135 at age 65 (approx. 2% [$8263] less than the initial projected accumulation value without an LTC rider). The projected income using withdrawals to basis and standard loans will be $53,088 per year (approx. 3.7% [$1992] less projected annual income than without an LTC rider) from ages 71-85.

Adding the LTC Rider in this scenario does not have much of a financial impact on the values above, however, it is important to keep in mind that the insured cannot take income and LTC benefits at the same time. Additionally, any distributions from the life policy will reduce future LTC benefits. This could impact the way you position the sale for your client. Please remember that the accumulation and income projections are not guaranteed, and the values are based on the future returns of the indexes chosen, so costs/charges may have a more substantial impact on both scenarios.

Protection Solutions

Again, let’s assume a 52-year-old male with a Preferred NT rating and a life pay policy with a $1,000,000 death benefit and coverage to age 121. Index Universal Life (IUL) policies are run at 5.50% and the Guaranteed Universal Life (GUL) is fully guaranteed to age 121.

In my opinion, Protection-based products are better suited for adding LTC/Chronic Riders. Protection products offer more design flexibility and, since they are not run for income, the death benefit can be applied to LTC expenses, assuming the client qualifies. AgencyONE offers quite a few options with a specified death benefit and allocates a portion of the death benefit to the LTC pool – for example – $500,000 of LTC coverage on a policy with a $1,000,000 death benefit.

The following Protection-based options are from 3 of our Carrier Partners. The first group is priced without an LTC Rider while the second includes a rider:

Options without LTC Rider

Assume: $1,000,000 of death benefit

CARRIER A: Solve to age 121. IUL rate – 5.5%. $10,025 annual premium. Policy guaranteed to age 90.

CARRIER B: Solve to age 121. IUL rate – 5.5%. $10,604 annual premium. Policy guaranteed to age 87.

CARRIER C: Policy guaranteed to age 121. $11,238 annual premium.

Options with an LTC Rider

Assume: $1,000,000 of death benefit with a $20,000 monthly LTC benefit for 50 months

CARRIER A: Solve to age 121. IUL rate – 5.5%. $11,448 annual premium. Policy guaranteed to age 90. Annual premium is $1,423 higher- 14.19%.

CARRIER B: Solve to age 121. IUL rate – 5.5%. $11,382 annual premium. Policy guaranteed to age 87. Annual premium is $778 higher – 7.34%.

CARRIER C: Policy guaranteed to age 121. $13,065 annual premium.Annual premium is $1,827 higher – 16.26%.

Let’s consider a possibly better and more affordable option that still includes LTC Coverage.

Assume:$1,000,000 of death benefit with $500,000 of LTC Benefit – $10,000 monthly benefit for 50 months

CARRIER A: Solve to age 121. IUL rate – 5.5%. $10,846 annual premium. Policy guaranteed to age 90. Annual premium increases by $821 compared to the no LTC Rider option – 8.19% but $602 less than the increase in premium stated above.

CARRIER B: Solve to age 121. IUL rate – 5.5%. $10,993 annual premium. Policy guaranteed to age 87. Annual premium increases by $389 compared to the no LTC Rider option – 3.67%but $389 less than the increase in premium stated above.

CARRIER C: Policy guaranteed to age 121. $12,701 annual premium. Annual premium increases by $1,463 compared to the no LTC Rider option – 13.02% but $364 less than the increase in premium stated above.

While the above information is based on just one pricing cell, the example helps to show where the value lies in product and design. With your clients who have larger cases, consider allocating some of the death benefit towards LTC instead of the whole face amount. It still provides good value to the client AND helps keep the cost of the overall policy down. AgencyONE works closely with our Advisors and considers including these riders in certain case models to determine if the added value justifies the cost.

Contact AgencyONE’s Case Design Department at 301.803.7500 for more information or to discuss a case.

‘Tis the Season and this ONE Idea Recap is very timely indeed, given the topics! People are particularly price-conscious all year but especially during year-end. We have a November ONE Idea from Case Design that discusses budget-friendly coverage that might be “just the gift” to consider for your clients this season. Additionally, lots of highly advanced tech will be gifted this year, but the human touch is still critical for success in personal and business relationships. The November Advanced Markets ONE Idea dives into the important insurance tech advancements but argues that it can never replace human involvement. Finally, a little weight gain during the holidays is a reality for many. Our Underwriting ONE Idea discusses the advancements in prescription medicine for weight control and how it has benefited clients and medical underwriting.

We hope our latest ONE Ideas have offered you guidance, inspiration, and at least one idea. With that in mind, the following is a recap of our ONE Ideas for the month of November.

AgencyONE started the month with an article from Craig Baumgartner, RICP titled“A Solution to Lock in Chronic Illness Coverage on a Budget”. This piece did a great job showing the progression of a case and optionality when the goal is for both death benefit and living benefits coverage BUT the client’s budget is driving the case. We worked with the AgencyONE 100 Advisor to determine exactly what the client needed and could afford. The Case Design team and advisor considered initial options which were great choices but turned out to be too expensive for the client who had two children still in college. Ultimately, the client agreed to an excellent and affordable solution that locked in insurability for a future policy conversion tailored to the client’s needs! Make sure to check out the detailed case study included in this ONE Idea.

Our second ONE Idea for the month was written by Gonzalo Garcia, CLU and was titled “When Technology Needs a Human Touch! A Commentary on Web-Based Life Insurance Platforms”. Gonzalo’s commentary applauds the firms that are working hard to develop and embrace technology that is changing the dynamics of the life insurance industry. He focuses, however, on the importance and irreplaceability of human interaction and expertise that is required for the many cases that do not fit neatly into a box. A professional human “touch” remains critical to the specialized handling and strategic placement of your cases. Make sure to read the full article for all of Gonzalo’s insights.

Our final ONE Idea for the month was from our Underwriting Department and penned by Dennis Bartos, PA. While Dennis’ article “I Wanna New Drug – Underwriting Weight Loss” humorously refers to a Huey Lewis tune from the 80’s, the article and case study address the serious impact that the new weight loss drugs like Ozempic have had on the health and life insurance underwriting of those prescribed and using the drugs. We recommend you read the full article to see how your clients might benefit from the knowledge base that AgencyONE’s Underwriting Team possesses.

Our AgencyONE 100 Advisors have been working hard all year but especially this last quarter to get their year-end business processed and completed. Trust that AgencyONE is hyper-focused and working diligently to move these cases into the “paid” column.

We are dedicated to helping you with any of your last-minute FORMAL business. AgencyONE and our carrier partners have switched to focusing on FORMAL APPLICATIONS ONLY! Don’t forget to consult the year-end business guidelines and deadlines published by our carrier partners on the AgencyONE website under your Advisor Dashboard.

You can find our most recent ONE Ideas under “Updates > Blogs” on our website homepage. Additionally, a full library exists on your personal Dashboard on our website under the Sales/Marketing tab (you must have a website login for access to the complete library). If you see a ONE Idea you like, we will happily brand it for your company. Just let us know.

AgencyONE provides these ONE Ideas to help you and your clients gain a better understanding of the planning, product selection, design, and underwriting that goes into the purchase of life insurance (with and without linked benefits), annuities and disability insurance. We hope you find these ONE Ideas helpful when assisting your clients with their financial, wealth, business, and estate planning needs.

Please contact AgencyONE’s Marketing Department at 301.803.7500 for more information

")

")

")

")

")

")