")

Hidden 1035 Opportunities: Don’t Miss out on Creating Joint Benefits!

Our Case Design team is often asked to review inforce policies for our AgencyONE 100 advisors and clients who are looking for solutions that will better utilize existing policy cash values to satisfy a different planning need. Opportunities for replacement often focus on adding a benefit that does not exist with the current coverage – anything from paid up death benefit to guaranteed income to living benefits. This week’s ONE Idea will explore some lesser-known options to consider and the rules and the work-arounds available for your clients who want to create joint benefits by exchanging an individual policy.

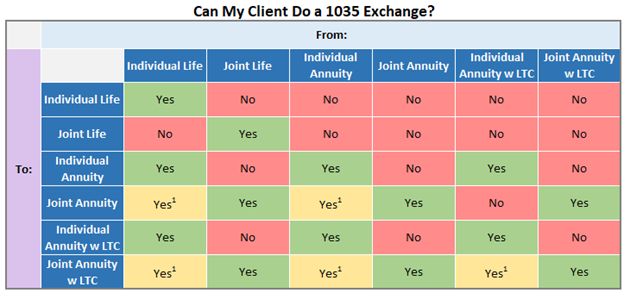

Section 1035 exchanges are a powerful tool lent by the IRS to help clients exchange one life or annuity policy for another without any taxable recognition of gains or losses. One limitation of the rule, however, is that exchanges must be like-to-like: ownership as well as the insured(s)/annuitant(s) must match from the original policy to the replacement. Additionally, 1035 exchanges from life insurance to annuities can be accomplished, while the opposite is not true. The table below displays the existing exchange rules.

While these rules are mostly straightforward, there exist a few hidden workarounds that can unlock additional JOINT benefits when exchanging an individual life or annuity policy. By knowing these rules, you can help your clients reach their goals and add value by being a subject matter expert!

Scenario 1 – Your client’s current life insurance or annuity policy has grown significantly, but now it’s time to think about taking income.

Josh (male, age 62) is the current owner of a participating whole life policy that was written on him as a child. His grandparents generously paid for a cash-rich paid-up policy that has grown over the years with dividends and paid-up additions. Josh now has other more cost-effective death benefit coverage inforce and is looking for alternative uses for his whole life policy’s approximately $500,000 of cash value.

He has looked into taking income tax free distributions from his whole life insurance policy but has heard horror stories about how unmanaged contracts can accrue large loans that must be addressed later, a risk he is not willing to take. Ideally, Josh would use this policy to create a floor of guaranteed income for him and his wife Beth (female, age 61). Having a guaranteed income base would allow his AgencyONE 100 advisor to invest his other assets more aggressively. Knowing that it is not possible to 1035 an individual life policy to a joint SPIA, Josh’s advisor gives AgencyONE a call looking for solutions.

He has looked into taking income tax free distributions from his whole life insurance policy but has heard horror stories about how unmanaged contracts can accrue large loans that must be addressed later, a risk he is not willing to take. Ideally, Josh would use this policy to create a floor of guaranteed income for him and his wife Beth (female, age 61). Having a guaranteed income base would allow his AgencyONE 100 advisor to invest his other assets more aggressively. Knowing that it is not possible to 1035 an individual life policy to a joint SPIA, Josh’s advisor gives AgencyONE a call looking for solutions.

The Workaround: Fixed indexed annuities these days often have optional lifetime income with the flexibility to elect lifetime guaranteed income when it best suits the client. The client can turn on the lifetime income stream immediately after issue or defer and let the annual income grow. Access to cash value, comparable payouts, flexible deferral, and higher commissions make such products attractive SPIA alternatives. An additional benefit is that the income rider can often pay based on joint lives when a spouse is listed as the sole primary beneficiary.

Options for Josh, the client:

- Option 1: Individual indexed annuity with lifetime income rider – a $30,900 lifetime annual income amount is available immediately after issue – based on Josh’s life only

- Flexibility to defer income and take a larger annual amount later (ex: $51,750 after 5 years; $75,600 after 10 years)

- Retains access to policy’s cash value which continues to increase based on underlying index performance

- Option 2: Individual indexed annuity with a joint lifetime income rider – $27,300 lifetime annual income amount is available immediately after issue – based on joint lives

- Flexibility to defer income and take a larger annual amount later (ex: $46,350 after 5 years; $68,400 after 10 years)

- Retains access to policy’s cash value which continues to increase based on underlying index performance

Because of Beth’s younger age and longer life expectancy, the couple ultimately chose option 2 which creates a lifetime income stream based on Beth’s age.

Scenario 2 – Your client’s current life insurance or annuity policy has grown appreciably but he has reached out to you and requested help minimizing the impact of the taxable gain.

Scenario 2 – Your client’s current life insurance or annuity policy has grown appreciably but he has reached out to you and requested help minimizing the impact of the taxable gain.

Ryan (male, age 64) had a $25,000 windfall at age 30. On the advice of a family financial advisor, he invested the lump sum in a variable annuity and hasn’t thought much about it since. Now, at age 64 the cash value of the policy has increased to $250,000. He likes seeing the cash value number grow on his annual statements every year, but at the same time, the liability of $200,000+ of taxable gains has made him hesitant to take any action.

The AgencyONE 100 Advisor recalled a ONE Idea about how annuities with long term care benefits can potentially eliminate tax liabilities but wonders if there is anything that can be done to provide joint LTC benefits for Ryan and his wife Sarah (female, age 65). The advisor knows they cannot directly 1035 an individual annuity to a joint annuity and reached out to AgencyONE for some additional solutions.

The Workaround: One of AgencyONE’s annuity/ LTC carrier partners has run into this situation before and developed a workaround that can provide joint long term care benefits. The new like-to-like policy was issued with the same individual owner and annuitant, but crucially with a provision to add Ryan’s wife, Sarah, as the sole primary beneficiary and as an “eligible person” for LTC benefits.

Options for Ryan, the client:

- Option 1: $10,520 initial monthly LTC benefit with projected annual increases

- Individual coverage only

- 96 total months of benefit available

- Option 2: $8,251 initial monthly LTC benefit with projected annual increases

- Available for either or both clients (husband / wife)

- 102 total months of benefit available

- Option 3: $5,193 initial monthly LTC benefit with projected annual increases

- Available for either or both clients (husband / wife)

- Lifetime, uncapped pool of LTC benefits

All 3 options can potentially eliminate the income taxes otherwise due on gains when used to pay for LTC expenses.

Ryan and Sarah ultimately selected Option 3 – A Win/Win outcome! The AgencyONE 100 advisor’s solution addresses the issue of taxable gains in the policy – potentially eliminating taxes on the growth altogether! The solution also provides valuable long term care coverage for both Ryan and Sarah that they cannot outlive!

The AgencyONE Case Design team is well-versed in these options, rules, and workarounds and available to assist you in looking for ways to help your clients turn old individual contracts into policies with joint benefits that better fit their current needs.

Contact AgencyONE’s Case Design Department at 301.803.7500 for more information

or to discuss a case.

")

")

")